Racial inequality in the United States has many dimensions, but one of the most impactful and broad-ranging is economic. On average, people of color experience significantly lower levels of income, retirement savings, and rates of homeownership than non-Hispanic white Americans. They also face different struggles while paying down student loan debt.

Making strides toward improving these issues, let alone solving them, is far from simple. But a first step is acknowledging and understanding the magnitude of the problem.

Here are some key statistics about the impact of the racial divide for income, savings, and overall financial well-being. (You can find a full list of the stats in this previous article.)

- Income and Poverty

- Homeownership Rates and Value

- Student Loan Repayment

- Savings Rates

Income and Poverty

While the racial wealth gap is the result of multiple factors, a disparity in income is likely the clearest indicator of how wide it truly is.

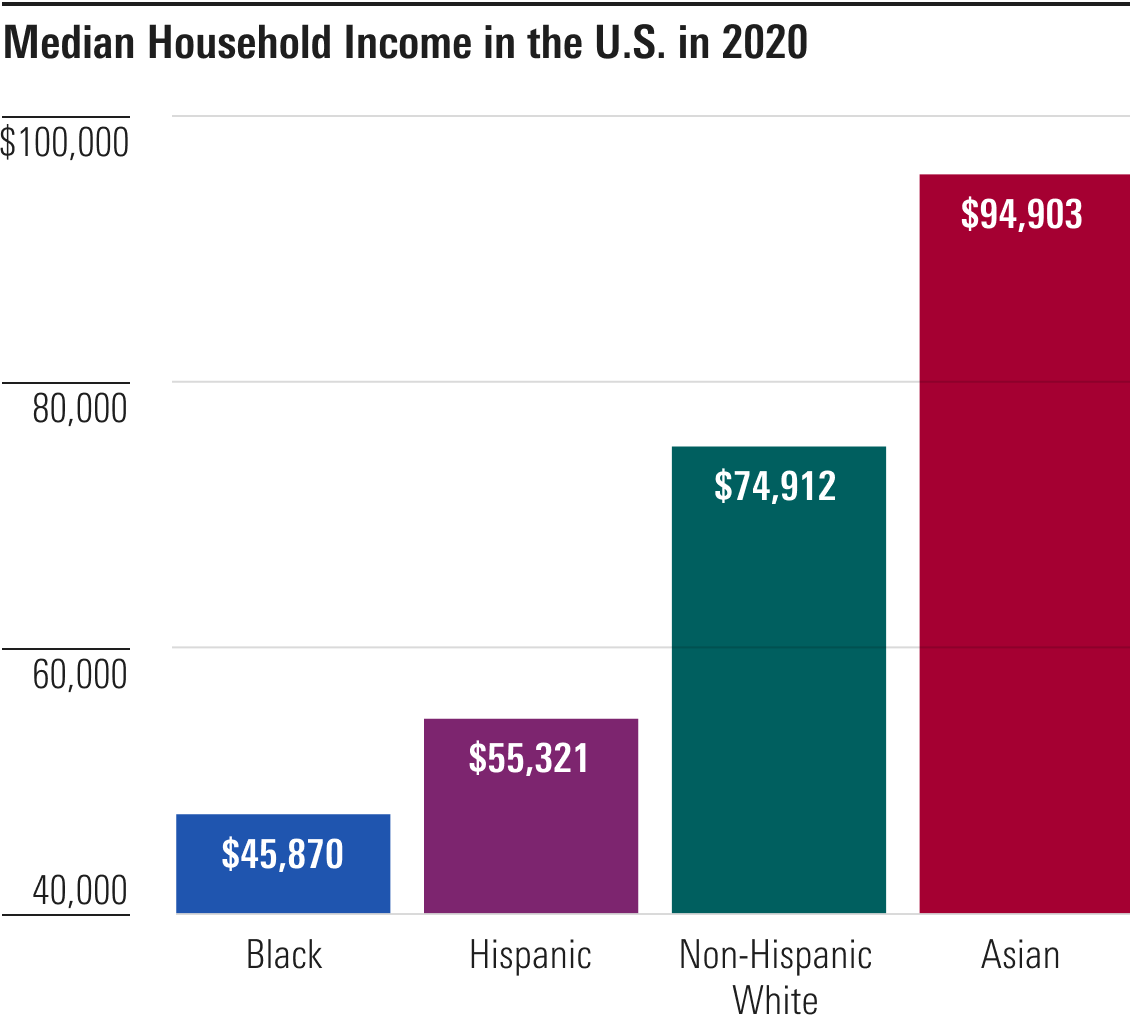

In 2020, the median non-Hispanic white household made nearly $75,000, compared to just over $45,000 and $55,000 for Black and Hispanic households, respectively. To paint this picture more clearly, Black and Hispanic households respectively earned 61% and 74% of the income of every median non-Hispanic white household in 2020, according to the U.S. Census Bureau.

Income gaps between races in America make it much more difficult for people of color, particularly across generations, to build more wealth.

One policy solution that could potentially help close this gap is an idea called “baby bonds,” originally proposed by two academics: Darrick Hamilton and William Darity.

In simplest terms, the government would contribute to savings accounts for children under 18, with the contributions determined by family income or wealth. When a recipient turns 18, the money can go toward certain uses, such as paying for college or buying a house.

At Morningstar, we believe it is important to use our expertise to analyze the effect such programs could have on reducing the racial wealth gap and the trade-offs in how such programs are designed.

Poverty can take on many forms. It’s not always as obvious to identify as one may think, meaning that it could also be far more common than expected.

Based on the stipulations established by the U.S. Census Bureau, the threshold to determine if a family of four technically lives in poverty in 2020 was an income of $26,246. (In 2019, this number was $25,926.) Now, compared to the average cost of living in much of the country, it’s debatable whether or not this low of a threshold is an accurate and realistic threshold.

According to the 2020 census, Black Americans were more than twice as likely to be living in poverty than non-Hispanic white Americans. Hispanic Americans weren’t very far behind.

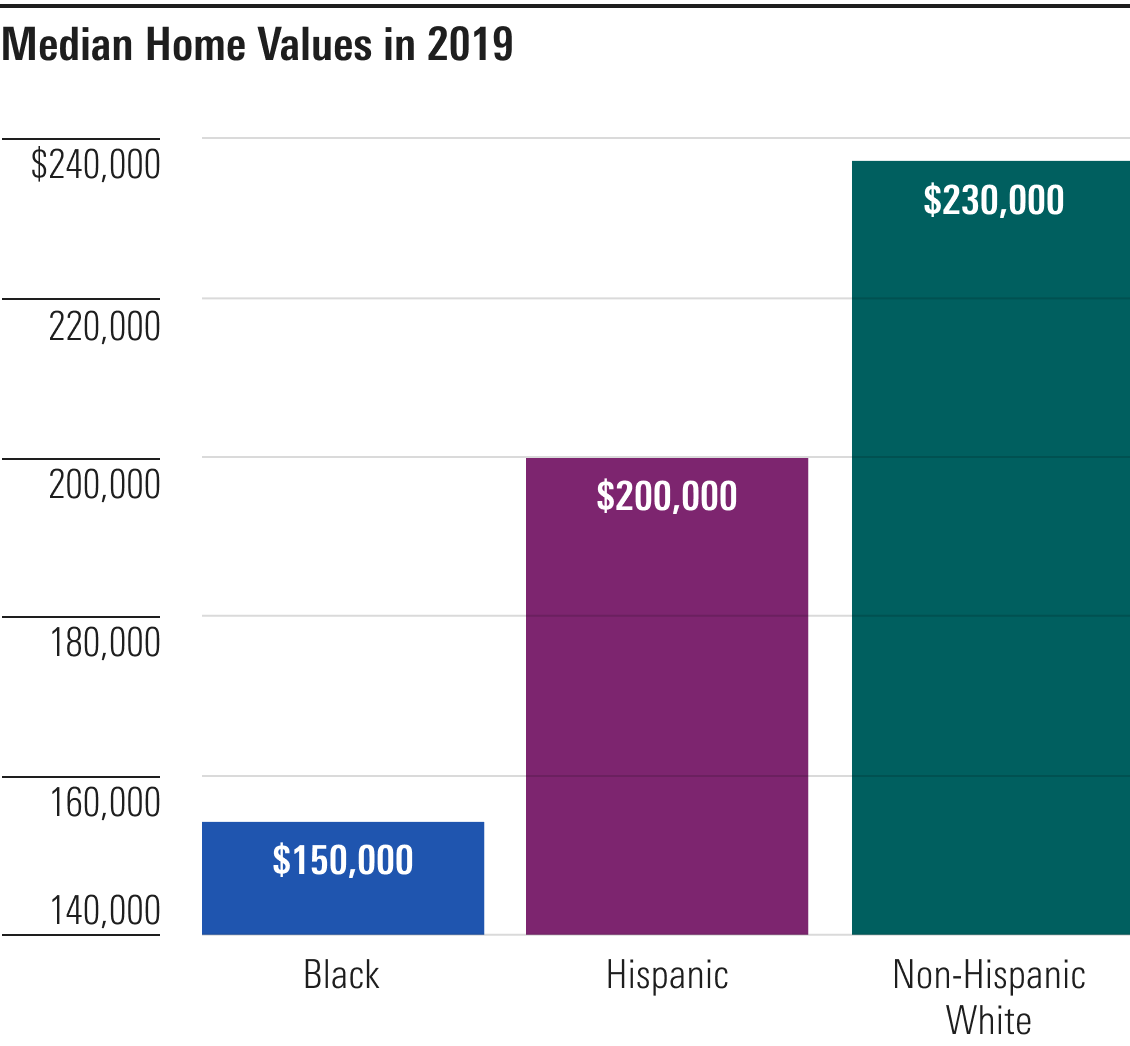

Homeownership Rates and Value

Homeownership has long been considered a vital part of obtaining upward financial mobility.

But how effective can homeownership be at wealth building when pursuing it can leave certain segments of the population with higher levels of debt and lower returns?

As of 2019, the gap between homeownership rates, net worth, and median home values of Black and Hispanic households compared to non-Hispanic white households may be the vastest ones recorded.

Perhaps, if the homeownership gap closes, it will truly be a way for all families to build and pass down wealth across generations.

https://view.ceros.com/morningstar/article-racialwealthgap-exhibit5

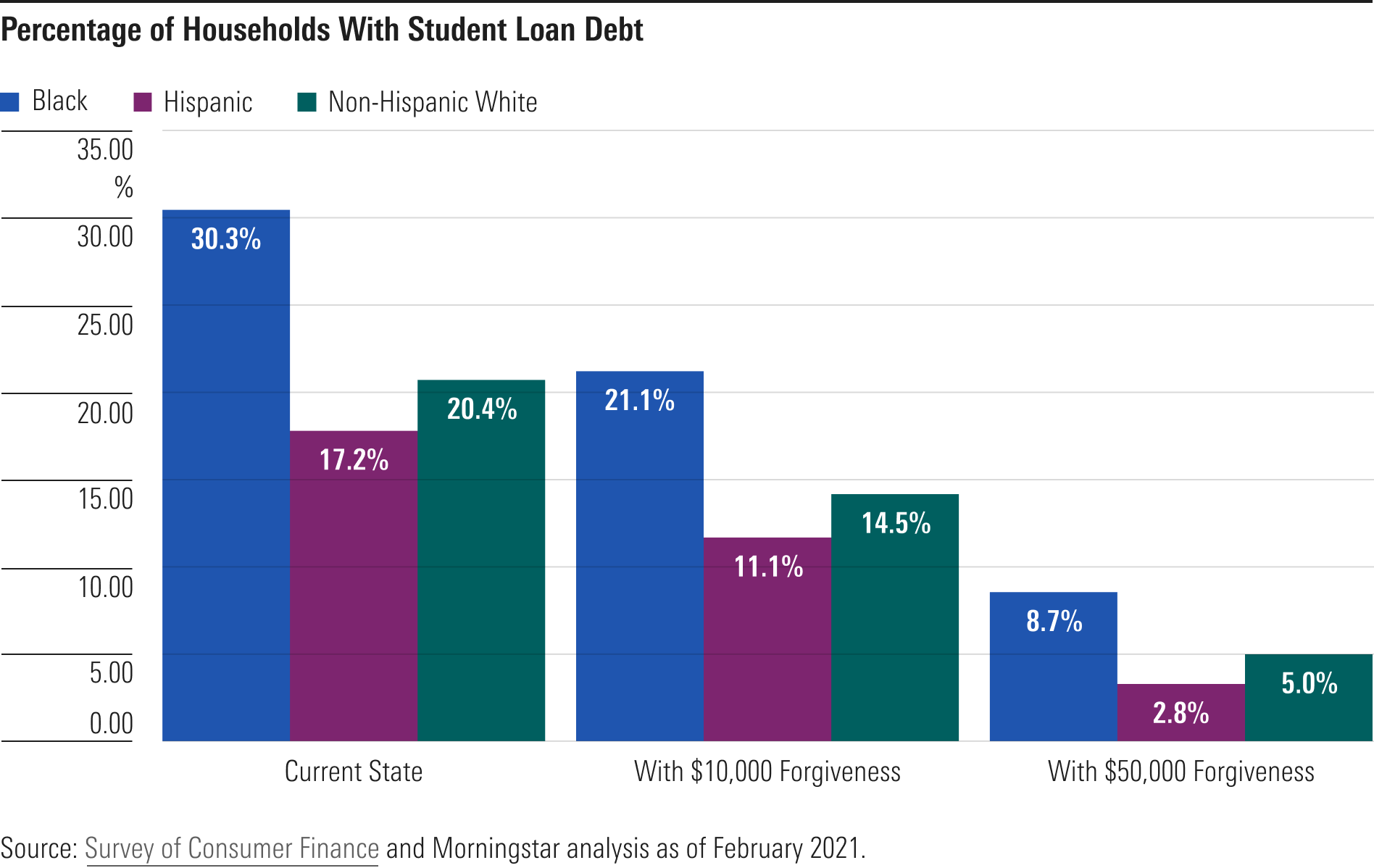

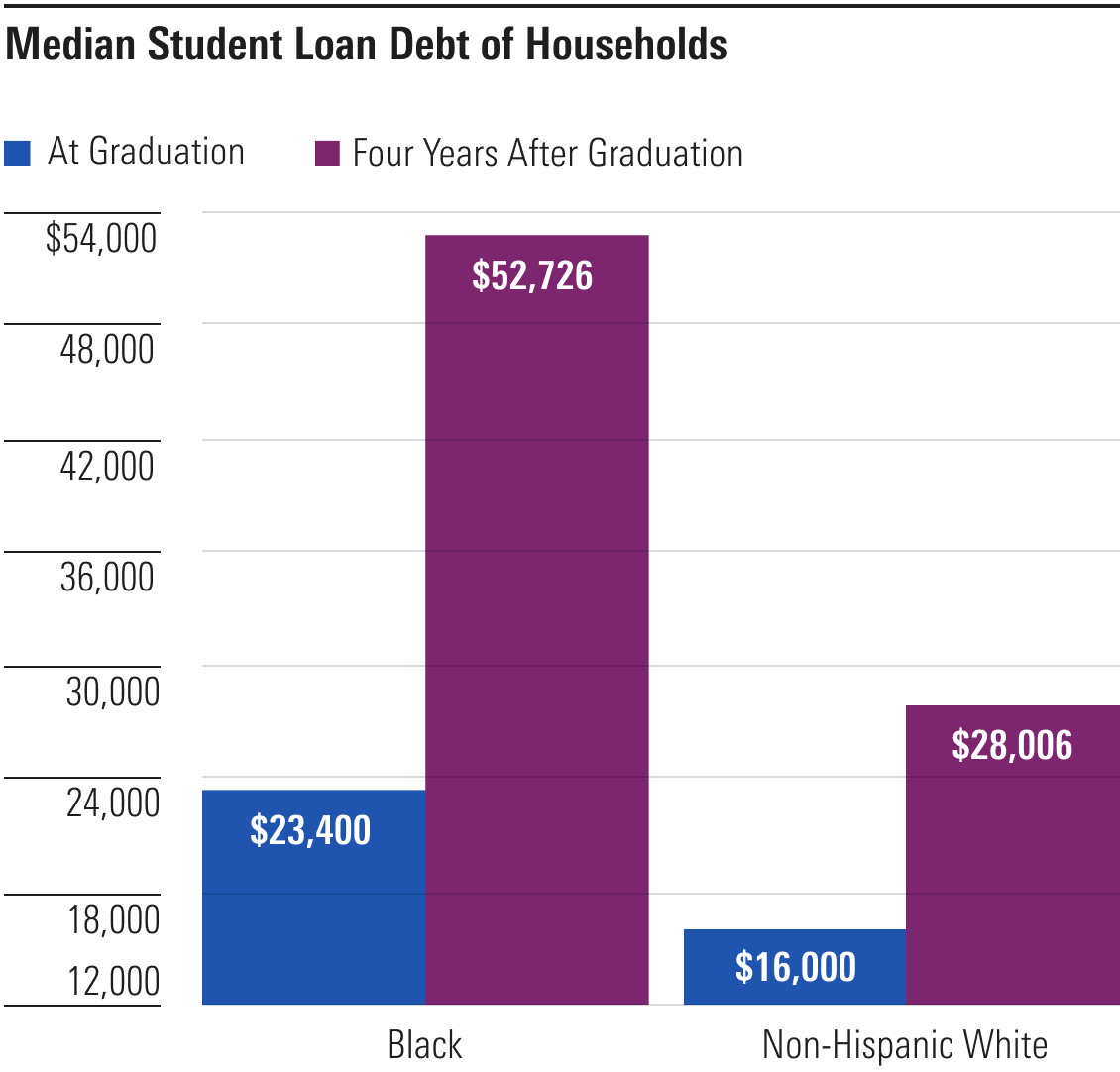

Student Loan Repayment

According to data from the Survey of Consumer Finances, nearly one third of households in the U.S. have student loan debt. But the average Black household has more to pay off than other households.

And, if trends that the Brookings Institution first published in 2016 still hold true, Black college graduates still owe considerably more than non-Hispanic white graduates four years after college due to factors such as interest accrual and graduate school borrowing, which is part of why student loan forgiveness has been discussed so widely in recent years.

We recently looked at the breakdown of households with student loan debt by income quartile now, as well as these breakdowns after $10,000 and $50,000 of loan forgiveness, to see what impact it could have.

Looking at the changes in the lowest and highest income quartiles, $10,000 forgiveness removes student debt for 34% of households in the lowest quartile and 29% of households in the highest quartile.

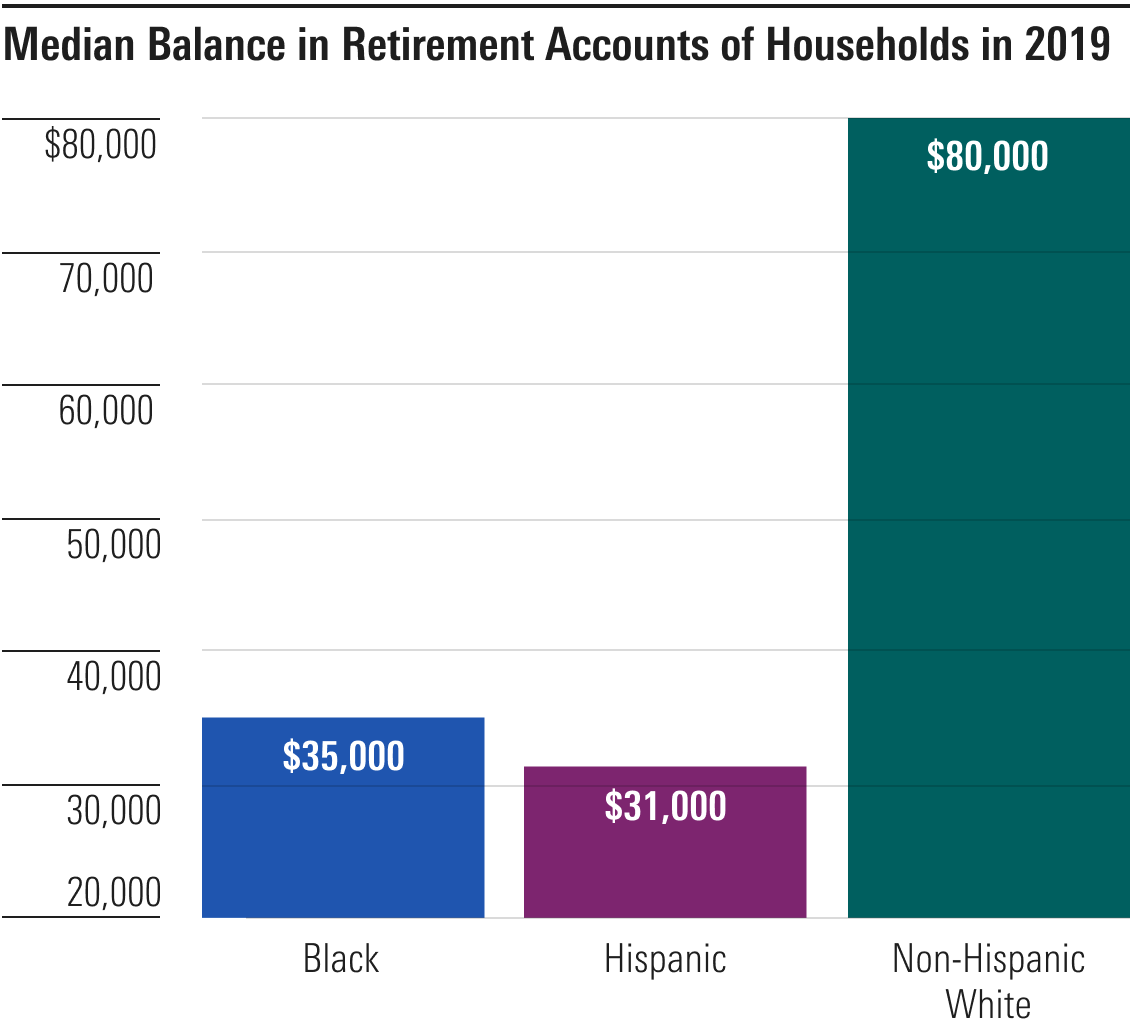

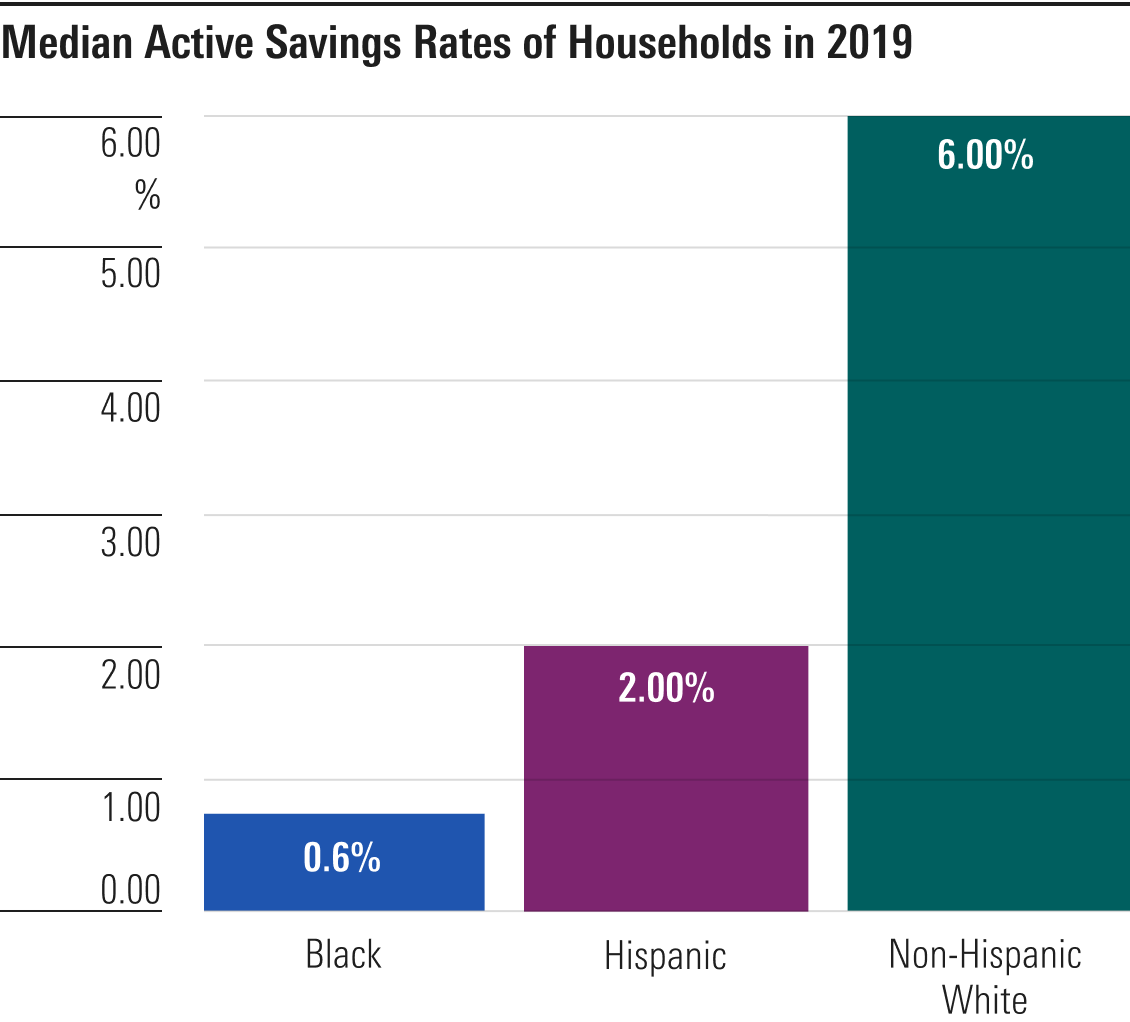

Savings Rates

Saving, in general, is something that a lot of Americans can improve. There are even differences in how people save based on which parts of the country they live in. But that’s even more the case when it comes to saving for retirement.

While many savvy investors can aim for a goal such as having seven figures saved up by the time they retire, others are nowhere close. And the shortcoming in saving is even more drastic for Black and Hispanic families.